To outperform the lots, we should take extra danger than common. A technique to take action is to put money into enterprise capital. Nevertheless, enterprise capital is a type of affected person capital, and affected person capital requires time. That’s the one useful resource older traders have much less and fewer of.

At 50 in mid-2027, I am getting into the previous man part of my life. It is unhappy, however the common 50 12 months previous American male is roughly 65% of the way in which by way of his life expectancy. The time horizon math begins working towards you in methods which are straightforward to disregard till you sit down and really do it.

As somebody who allocates as much as 20% of investable property into different investments together with enterprise capital, enterprise debt, and industrial actual property, I am discovering it more and more arduous to justify committing to a brand new enterprise capital classic.

Since 2018, I’ve invested with a conventional VC agency that lately raised a brand new AI devoted fund in 2026. The Common Companion is a good friend of a good friend. I’ve the choice of investing between $100,000 – $1 million of their family and friends spherical. The query is whether or not I ought to at my age, and if that’s the case, how a lot.

Possibly you are older and going through this similar dilemma proper now. You see SpaceX lastly IPO and do not wish to miss the subsequent rocketship. As a result of what is the level of constructing extra wealth if you cannot take pleasure in it for the subsequent 10 or so years?

The Issue Of Investing In Enterprise Capital When You are Older

If I put money into a conventional enterprise capital fund in 2026, the timeline appears like this:

- Meet capital calls over the subsequent three to 5 years: 2026 by way of 2030

- File Okay-1s for my taxes for the subsequent 8-11 years

- Probably obtain all capital again plus income someplace between 12 months 8 and 12 months 11

If the 2026 classic efficiently returns capital and income in 11 years, I will be 60. So the central query turns into: will I truly be round, and wholesome sufficient, to take pleasure in it?

I would wish to assume so. However I would assign roughly a ten% likelihood I will not be alive at 60, and an extra likelihood that I will be alive however coping with a well being difficulty that makes cash much less helpful than time. NASCAR legend, Kyle Busch, sadly died at simply 41, so that you by no means know when your final day will likely be. Please benefit from every minute.

All my self-discipline of assembly capital requires 5 years and delaying gratification for 11 years could finally profit my kids, who will likely be 20 and 17, and my spouse, who will likely be 57. That is factor as the principle monetary supplier. Nevertheless, it additionally means I will not be capable to spend it on them within the current.

Notice: For those who’re trying to get an reasonably priced time period life insurance coverage coverage, try Policygenius. Each my spouse and I received matching 20-year time period life insurance coverage coverage and felt an incredible quantity of reduction afterward. Defend our youngsters and their futures. Policygenius supplies you no-obligation, aggressive, and customised quotes multi function place so you do not have to buy round.

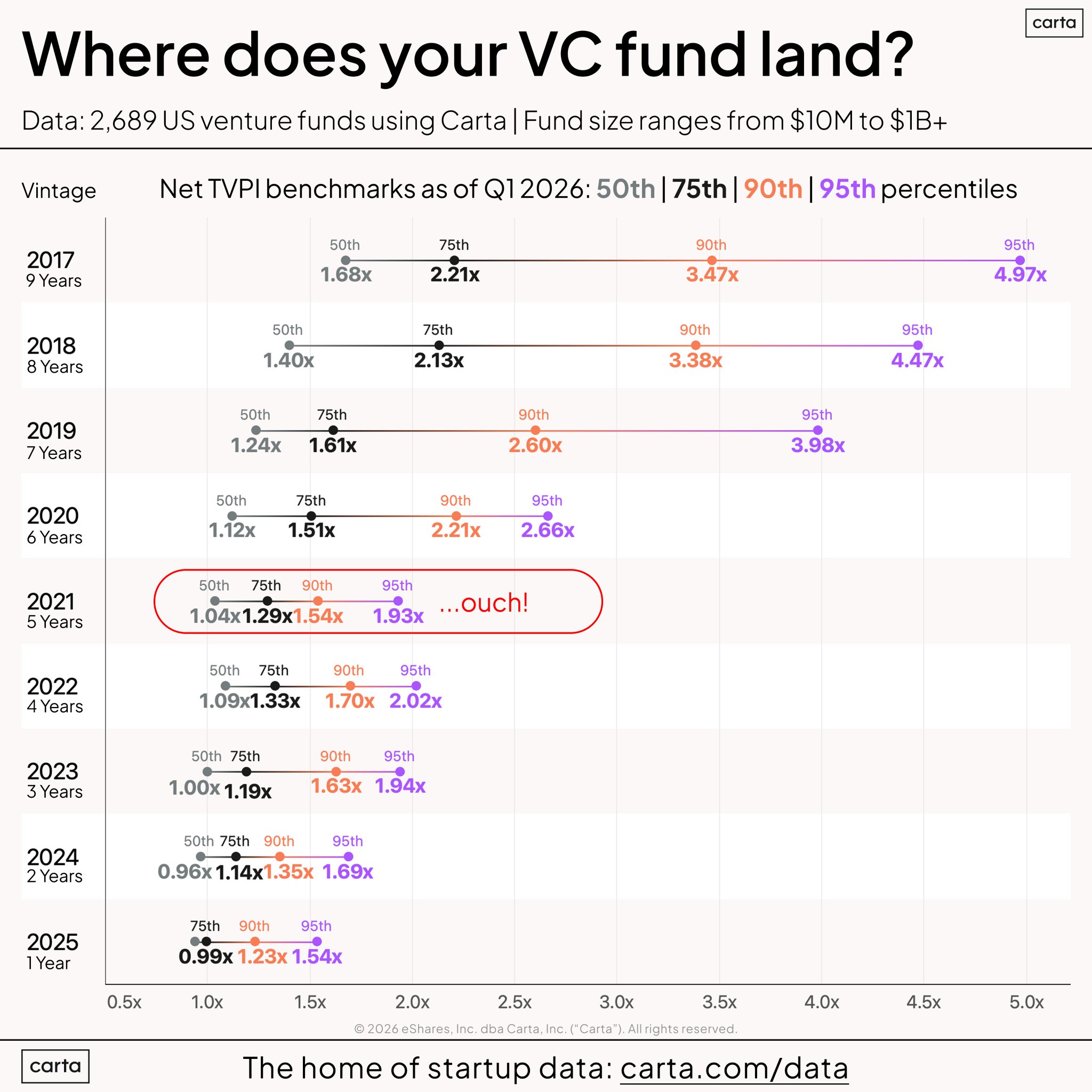

What VC Returns Truly Look Like, And What They Do not

Earlier than deciding whether or not to put money into VC at any age, it helps to be clear-eyed about what the asset class truly delivers.

The highest-quartile VC funds, those you examine and those everybody desires entry to, have traditionally generated web IRRs of 20 to 30%+ over a full fund cycle. The median VC fund? Roughly 8 to 12% web IRR, which is analogous to the S&P 500’s historic common of round 10%, and that is earlier than accounting for illiquidity.

In my very own expertise since I began investing in enterprise within the early 2010s, my returns have ranged from 8% to 40% IRR throughout funds. However in mixture, they have not dramatically outperformed the S&P 500. Few asset courses have given what a heater the S&P 500 has been on since 2012.

The actual fact is most individuals who assume they’re having access to top-tier VC are having access to median-tier VC. And median-tier VC, after 10 years of illiquidity and Okay-1 complications, is a questionable commerce. In the meantime, the NASDAQ is up 6.5X web previously 10 years.

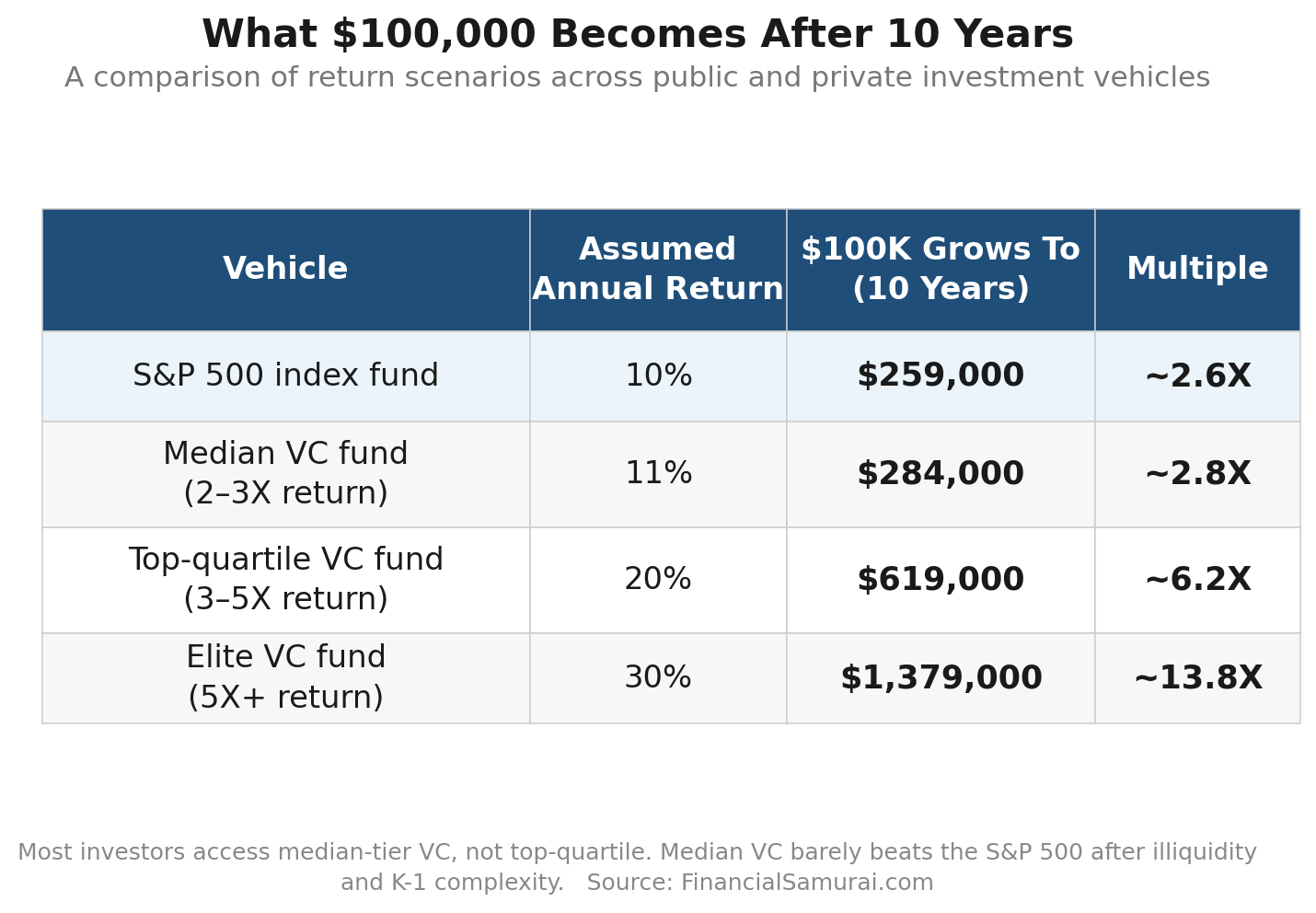

Future Returns Of Enterprise Capital Efficiency And The S&P 500 Over 10 Years

This is a tough comparability of how $100,000 compounds throughout completely different return eventualities over 10 years at numerous annual return percentages:

The S&P 500 quantity is offered to anybody, liquid at any second, with no Okay-1s, no capital calls, and no lockup. The highest-decile VC quantity is extraordinary however requires entry most individuals merely do not have. It is invite solely, and also you and I are nearly at all times by no means invited.

The reasonable VC situation for many traders sits in that center band, the place the illiquidity premium is skinny.

This is the reason entry issues a lot in enterprise. If you will get into the highest 10% of funds which have entry to the highest 1% personal firms, the illiquidity is probably going price it at nearly any age. These corporations embrace Sequoia, Benchmark, Founders Fund, Thrive Capital, Accel, a16, Bessemer Enterprise, Greylock Companions, Kleiner Perkins, Dollars, Index Ventures, and a number of other extra.

For those who’re in the course of the pack, the case weakens significantly, particularly as you become old. Therefore, chances are you’ll wish to scale down your allocation.

The Worth Of Liquidity Goes Up As You Age

Liquidity is just not a hard and fast worth. It’s price extra as you age, not much less. This is why.

Once you’re 30, an emergency like a job loss, a well being scare, or a market crash is painful however survivable. You’ve gotten a long time of future earnings forward. The illiquidity of a VC fund is a manageable constraint. It may truly be a constructive function because it forces you to speculate over the lengthy haul by way of down cycles.

Once you’re 60 and going through an aggressive most cancers prognosis, illiquidity is not a function. It is a cage. The cash you’d most wish to use, to take your loved ones on a once-in-a-lifetime journey world wide whilst you nonetheless have the power, is locked inside a fund you possibly can’t entry.

Or take into account a much less dramatic situation: your little one wants emergency surgical procedure overseas. Your aged dad or mum wants costly full-time care. You wish to assist a partner pivot careers, which can imply no dual-income for a 12 months or two. These are actual conditions the place tappable fairness issues enormously. With conventional enterprise capital, that fairness merely is not there.

Due to this fact, for conventional capital, you could solely make investments cash you do not want for 10+ years.

The choice, investing in publicly traded automobiles with personal firm publicity, closed-end funds, or particular person shares, preserves optionality. Sure, there’s extra day-to-day volatility in public enterprise capital funds like VCX. And also you should be cautious together with your entry factors. However the fairness is yours to deploy when life truly occurs.

In any case, the aim of investing is to really spend it on one thing that improves the standard of your life. If not, investing only for investing’s sake is ineffective.

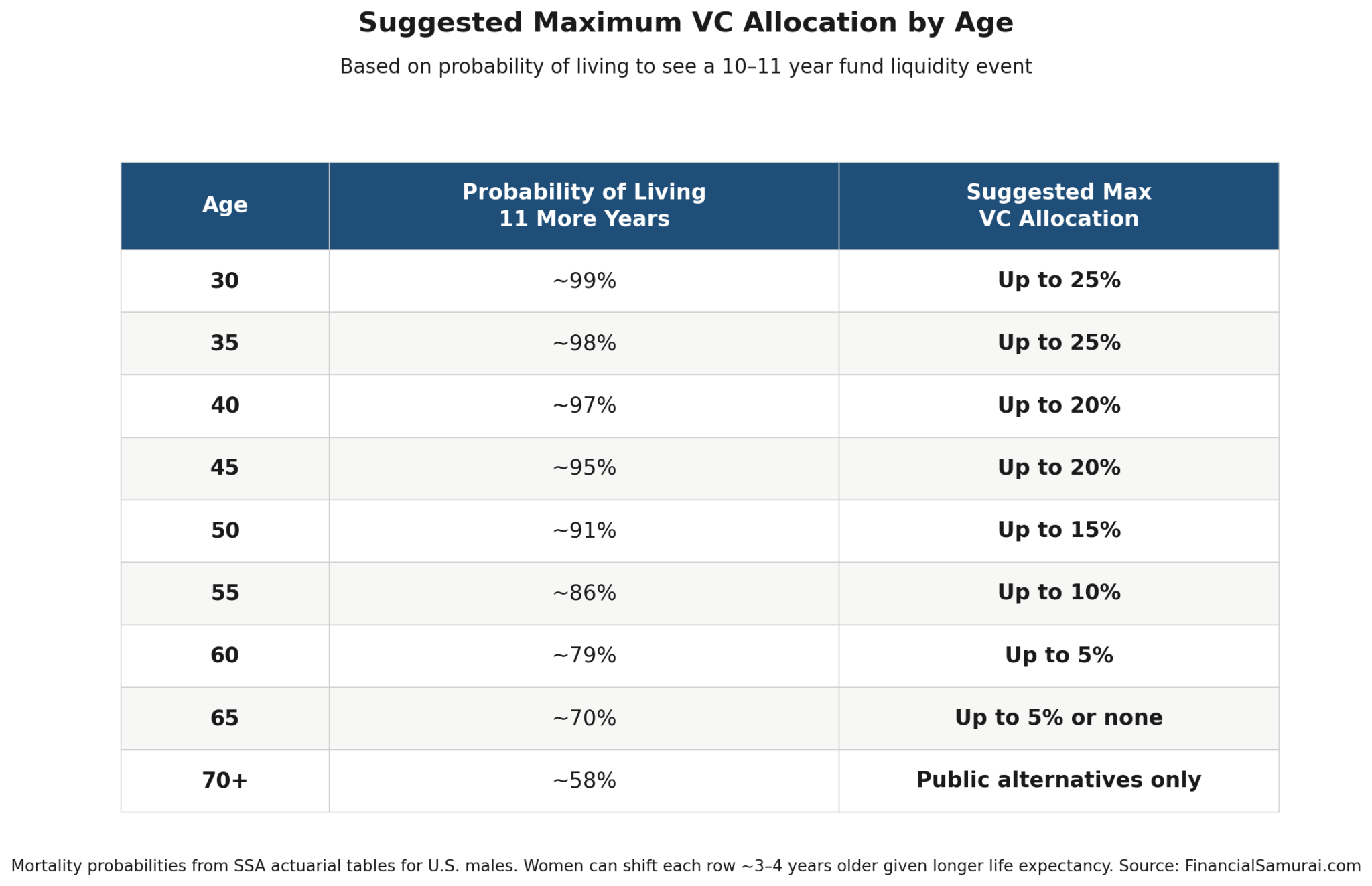

A Information: How A lot VC Ought to You Maintain At Every Age?

Let me provide a sensible framework for fascinated about your personal fund allocation as you age, grounded in two variables: your remaining life expectancy and the likelihood you’ll reside to see liquidity from a given classic. We’ll assume you will get right into a mid-tier enterprise capital fund or larger.

Given firms are staying personal longer, with extra features accruing to personal traders and staff, it is smart to allocate extra capital to personal investments.

Additional, in case your aim is to outperform the S&P 500 and obtain monetary freedom sooner, you should be keen to take extra danger for doubtlessly larger returns. There are two ranges of wealthy, and the richest did not get there by investing in index funds.

The Core Precept: Your VC Allocation Ought to Shrink As Your Time Horizon Does

A typical VC fund has an 8 to 11 12 months anticipated maintain. In case your planning horizon is 30+ years, a 10-year lockup is a minor inconvenience. In case your planning horizon is 12 to fifteen years, a 10-year lockup consumes most of it.

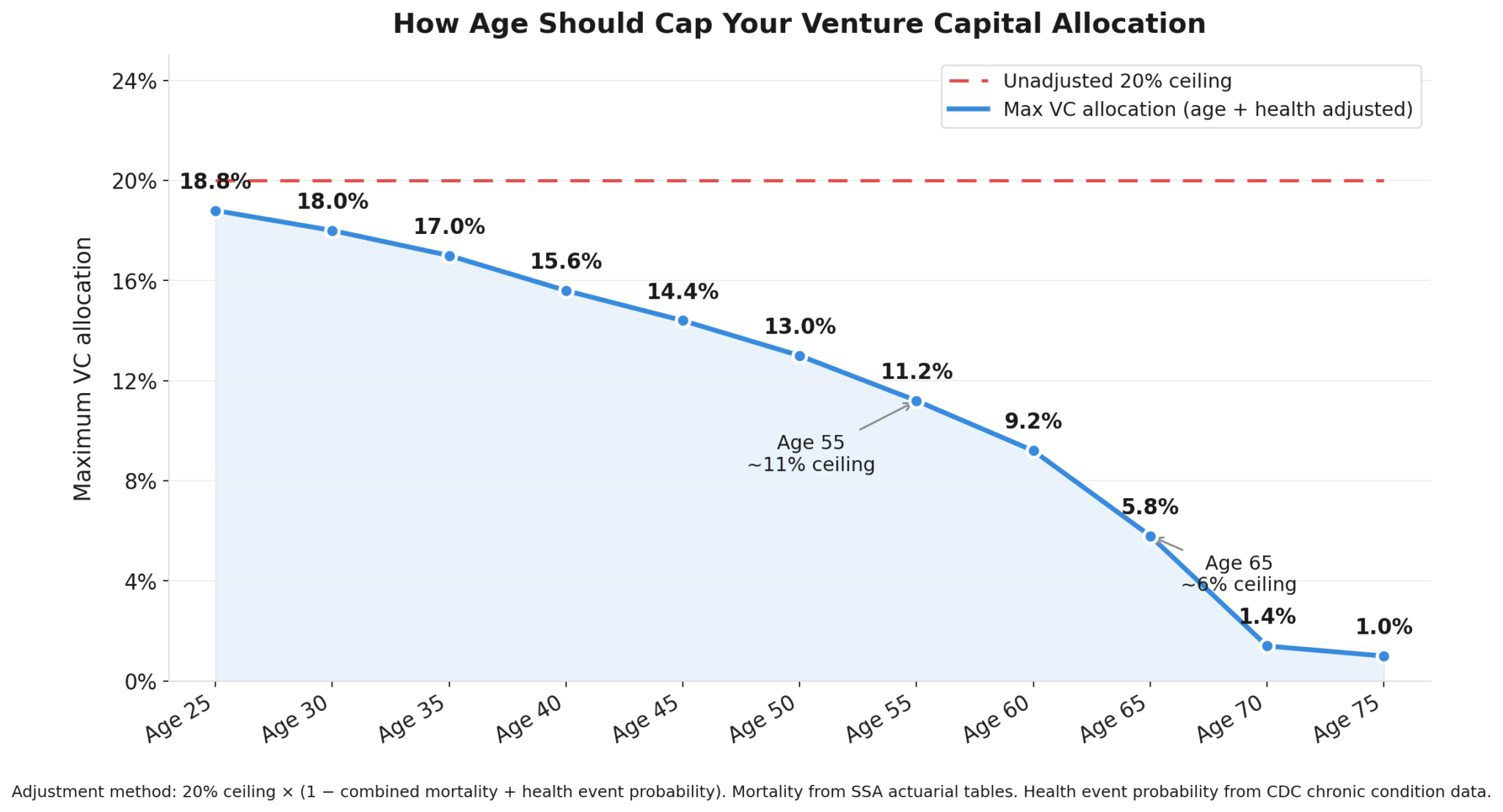

This is a urged most conventional VC allocation of investable property by age, assuming a 10-year fund:

*Mortality chances based mostly on SSA actuarial tables for U.S. males. Ladies can shift every row roughly 3 to 4 years older given longer common life expectancy.

Decrease Conventional VC Publicity The Older You Get

The logic is straightforward: your most VC allocation ought to roughly observe your likelihood of residing to benefit from the returns. If there is a 9% likelihood you will not be alive in 11 years, it is arduous to justify locking up 20% of your portfolio on that wager, whatever the projected returns.

The nice irony of enterprise capital is that this: entry is hardest once you’re younger, hungry, and have the longest time horizon to profit from it. By the point you’ve got constructed the connections, the popularity, and the capital to get into the very best funds, chances are you’ll be too previous to need the lockup. That is not a solvable drawback. It is simply the way in which it really works.

This is the reason the creation of public enterprise capital funds like VCX has created different for youthful and older traders alike who need publicity to enterprise capital with out sacrificing liquidity.

The Second Variable: Well being-Adjusted Liquidity Wants

Past mortality, issue within the likelihood of a significant well being occasion that may make liquidity priceless even in case you survive. By age 60, roughly 40% of Individuals are managing no less than one continual situation with significant out-of-pocket value. By 70, that determine climbs above 70%.

This is the reason I don’t advocate allocating greater than 20% to enterprise capital typically. For many traders, the true ceiling sits decrease when you account for age.

The rule of thumb: begin together with your 20% most, then haircut it by your mixed likelihood of dying or going through a critical well being occasion over a typical 10-year lock-up. The riskier your private scenario, the extra you trim the illiquid place.

Instance VC Asset Allocation As You Get Older

This is the way it works with a $3 million liquid portfolio and a 20% VC ceiling, which supplies you a $600,000 place to begin:

- Age 25: Minimal mortality and well being danger, so that you barely haircut in any respect and may method the complete $600,000.

- Age 45: A roughly 10% mixed danger trims you to about $540,000.

- Age 55: A mixed 44% danger (say a 14% likelihood of not being alive in 11 years plus a 30% likelihood of a significant well being occasion) cuts your adjusted ceiling to about 11%, or $330,000, roughly half the theoretical most.

- Age 65: A 26% mortality likelihood and 45% health-event likelihood produce a 71% haircut, dropping your ceiling to round 6%, or $180,000.

The upside potential of enterprise capital doesn’t change with age. Your potential to attend it out does. The youthful you might be, the nearer you possibly can responsibly get to the 20% ceiling, or perhaps even past it. The older you might be, the extra a inflexible illiquid place turns into a legal responsibility reasonably than a chance.

Associated: Enterprise Capital Funding Phrases You Ought to Know

Extra VC Asset Allocation Examples By Age

This is how hypothetical portfolios is likely to be structured with applicable VC publicity at completely different life levels:

Age 35, $1M Portfolio

- $200,000 conventional VC / personal funds (20%)

- $700,000 S&P 500 index funds (70%)

- $100,000 Treasury bonds / money (15%)

Age 45, $2M Portfolio

- $340,000 conventional VC / personal funds (17%)

- $1,260,000 S&P 500 index funds (63%)

- $400,000 Treasury bonds / money (20%)

Age 50, $3M Portfolio

- $390,000 conventional VC / personal funds (13%)

- $1,860,000 S&P 500 index funds (62%)

- $750,000 Treasury bonds / money (25%)

Age 58, $5M Portfolio

- $400,000 conventional VC / personal funds (8%)

- $3,100,000 S&P 500 index funds (62%)

- $1,500,000 Treasury bonds / money / liquid alternate options (30%)

Discover that as VC allocation shrinks, the freed capital strikes towards liquidity, into bonds, money, and liquid alternate options, not simply into extra equities. This displays the rising worth of accessible cash as your life circumstances turn into much less predictable.

Slowing Down My VC Investments Submit 50

In 2027, I will begin slowing down my VC investments to match my mortality.

I will make these investments by way of my revocable residing belief, as I at all times have, so my spouse and survivors can handle the property easily if I had been to die prematurely. Then I will meet capital calls as they arrive and hope for the very best.

After roughly 20 years of VC investing, I’ve come to genuinely admire the capital name construction. It saved me disciplined by way of the 2008 monetary disaster, the 2018 correction, COVID, and the 2022 downturn, forcing me to deploy capital at moments after I would possibly in any other case have frozen.

Investing for the long term is usually factor. Sadly, as economists like to say, in the long term we’re all useless.

Weighing The Value Of Illiquidity

As somebody who has lived in San Francisco since 2001 and loves the startup ecosystem, there’s one thing uniquely energizing about investing in creators as a creator myself.

There’s additionally much less investing FOMO once you’re already a enterprise investor, since you’re within the recreation reasonably than watching from the sidelines.

That stated, the VC outperformance has been actual however not transformative. Because the years move, I’ve to weigh that modest premium towards the rising value of illiquidity. More and more, that tradeoff makes much less sense.

My hope and expectation is that Fundrise, which is again to focusing totally on actual property, finally launches VCX II following the success of VCX I. Ideally one which raises capital privately, deploys it over 2-3 years, after which lists on the NYSE. If that occurs, I will be the primary to commit. Fundrise is a long-time sponsor of FS.

With the ability to put money into enterprise capital whereas sustaining liquidity is a strong mixture. This is hoping the asset class retains evolving in that route. However for now, let’s benefit from the SpaceX IPO for these of you bought in instantly or by way of a VC fund!

Reader Questions And Writer Background

Readers, what do you concentrate on investing in personal funds after age 50 with a 10-year or longer lockup? Is there an age at which you’d cease committing to enterprise capital or different illiquid personal funds? And for these of you who’ve been in VC for a decade or extra, has the illiquidity ever value you in a second once you genuinely wanted the money?

Background: I’ve invested in enterprise capital funds and personal firms since 2006. I’ve beloved entrepreneurship since elementary college, and finally grew to become an entrepreneur myself with Monetary Samurai in 2009, after 10 years in finance. This ardour is among the massive causes I’ve continued to reside in San Francisco since 2001, regardless of reaching FIRE in 2012. Two of my enterprise capital funds personal SpaceX, and each portfolio firm that IPOs is thrilling. However not all IPOs are successes.

To proceed constructing your wealth and navigating an unsure future, subscribe to my free weekly e-newsletter. Be a part of 60,000+ readers who get my newest insights on investing, actual property, monetary freedom, and extra, despatched straight to their inbox.

{kind=link}