In an try to higher perceive the potential {discount} or premium to NAV for the Fundrise Innovation Fund, I needed to look at Pershing Sq. Holdings, ticker PSHZF, listed on the London Inventory Change.

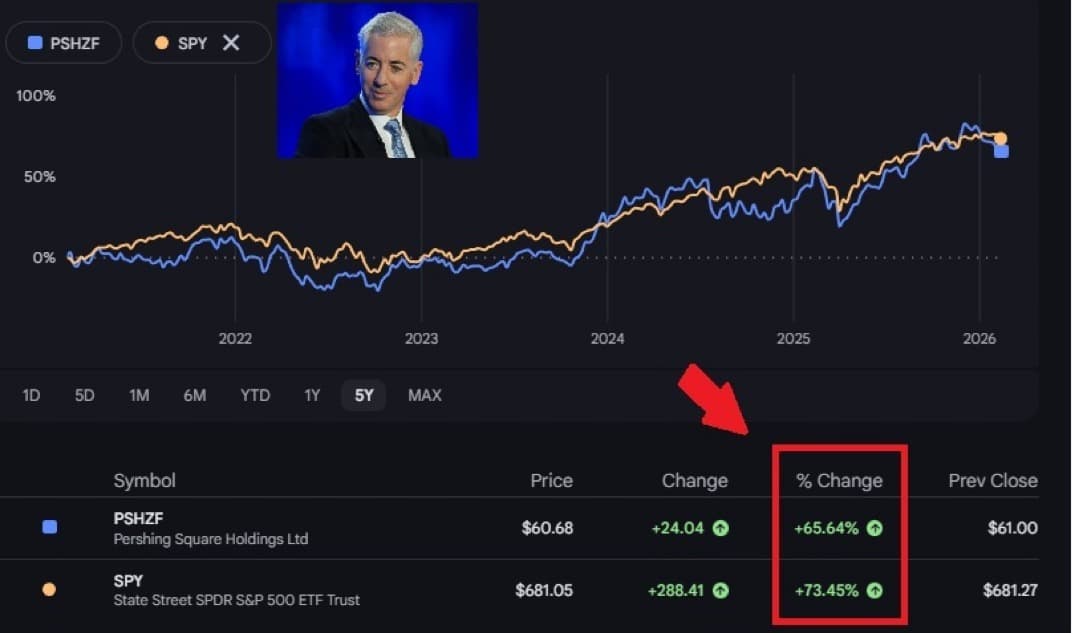

Pershing Sq. manages over $18 billion and is run by American, Invoice Ackman. In the meantime, the fund presently trades at a couple of 25% {discount} to its NAV. When it first listed in 2014, it traded at as small as a 9% {discount}. The NAV {discount} widened to about 40% in 2022, after which traded at a 30%–35% {discount} in 2023 and 2024.

As an investor, you possibly can take this -9% to 40% historic discount-to-NAV vary as a datapoint for when to speculate. Clearly, the higher the {discount} to NAV, the higher worth you might be getting. Not solely might the NAV rise in worth if Ackman invests in winners, however the {discount} to NAV might slender as properly.

If the Innovation Fund lists on the NYSE, might it commerce at the same {discount} to NAV as Pershing Sq.? It’s attainable, however I extremely doubt it for the explanations I spotlight on this put up.

Why Does The Pershing Sq. Fund Commerce At Such A Giant Low cost?

Listed here are 4 principal causes for such a persistent {discount} to NAV.

1) Core Holdings Are Public Equities

Pershing takes concentrated positions in 8–12 holdings and actively engages with administration to impact change. Previous holdings embody Chipotle, Restaurant Manufacturers Worldwide, Hilton Worldwide, Alphabet, Canadian Pacific Kansas Metropolis, and Amazon.

The difficulty with proudly owning public equities is that you and I can assemble the identical portfolio ourselves. In different phrases, there is no such thing as a barrier to entry to proudly owning public equities. Fund traders should depend on the acumen of Ackman and his analysts on when to purchase and promote.

Regardless of many of the positions being public equities, Ackman did use credit score safety to hedge draw back threat throughout the early 2020 COVID volatility. So in case you are investing in a hedge fund and wish draw back safety, Pershing can present that functionality. But it surely often does not appear to, going 90% – 100% lengthy.

2) Closed Construction + European Itemizing

PSH is a closed-end fund listed in London, not a ETF listed on a U.S. inventory alternate.

That creates:

- No each day redemption mechanism to arbitrage value again to NAV

- A restricted pure U.S. investor base that does not put money into LSE shares or funds

- Much less index inclusion versus U.S. funds

- Some institutional mandates that can’t personal foreign-listed Closed-end Funds (CEFs)

If this have been a U.S. ETF holding the very same portfolio, the {discount} doubtless wouldn’t practically be as massive. Perhaps 0-5% as an alternative. Closed-end funds can commerce at reductions for many years if there is no such thing as a catalyst to shut the hole.

Not like an ETF, there is no such thing as a easy mechanism forcing convergence, as I wrote in my put up on how completely different fund sorts commerce.

3) Payment Construction (1.5% + 16% Efficiency Payment)

PSH fees:

- 1.5% administration charge

- 16% efficiency charge above a high-water mark

That’s cheaper than conventional 2/20 hedge funds, however it’s costly relative to passive fairness publicity. In the meantime, traders mentally {discount} future returns as a result of charges compound.

While you {discount} anticipated future NAV development by charges, some traders demand a structural {discount}.

4) Focus Threat And Volatility

With often solely 8–12 shares within the portfolio, there may be important focus threat in PSH that warrants a reduction. Throughout good occasions, returns will be nice. However throughout unhealthy occasions, like in 2022, returns will be horrible, therefore the 40% {discount} to NAV.

In case you are investing in a hedge fund, your objective is often to scale back volatility and defend draw back threat via hedging (shorting some names). But when the fund doesn’t hedge meaningfully or persistently, and as an alternative creates further volatility for holders who should not fitted to it, a reduction to NAV is demanded.

With supervisor threat, key-man threat, and technique cyclicality, a reduction to NAV is barely pure.

Fundrise Innovation Fund Comparability To Pershing Sq. Holdings

Buying and selling at a 25% {discount} to NAV after a NYSE itemizing can be a horrible state of affairs for Fundrise Innovation Fund (VCX) holders. Nevertheless, I don’t suppose it should occur given the next variations in comparison with Pershing Sq. Holdings:

1) VCX Owns Non-public, Arduous To Make investments In Belongings

VCX owns extremely coveted non-public firm shares in names reminiscent of OpenAI, Anthropic, Databricks, Anduril, SpaceX, Canva, and extra. Not like public equities, only a few individuals can make investments straight in these corporations throughout their subsequent non-public fundraise. Consequently, it’s logical that traders would pay a premium to personal these names, not a reduction.

2) VCX Will Commerce On A A lot Bigger U.S. Change

VCX will attempt to listing on the NYSE, not the London Inventory Change. The NYSE is 8–9 occasions bigger than the LSE by way of whole market capitalization. Buying and selling quantity on the NYSE is usually $50–$100+ billion per day versus solely $5–$10+ billion per day on the LSE.

Consequently, the pure demand pool is bigger. VCX can be accessible to each U.S. retail brokerage account and will probably appeal to institutional flows.

3) VCX Costs A A lot Decrease Payment

VCX plans to cost a 2.5% annual administration charge and 0% carried curiosity (a proportion of income). PSH fees solely a 1.5% administration charge, however 16% of income after a high-water mark, which is a part of the explanation Ackman is so rich. I might a lot reasonably pay 2.5%–3% of AUM than 1.5% and 16% of income for corporations which have the potential to development tremendously.

Hypothetically, in case your $100,000 place doubles to $200,000 in a single 12 months, you’ll pay an roughly $3,750 charge to VCX and hold $96,250 of the income. In distinction, you’ll pay a $2,250 charge to PSH plus 16% of the $100,000 revenue, or $16,000, for a mixed whole charge of $18,250. Clearly, paying a $3,750 charge is preferable to paying an $18,250 charge.

4) VCX Manages A Smaller, Extra Nimble Fund With Extra Holdings

VCX is a ~$550 million fund versus PSH at $18+ billion. Consequently, it’s generally more durable to outperform with such a lot of belongings beneath administration.

For instance, investing $55 million (10% of VCX) in a personal development firm that performs properly could make an even bigger distinction to VCX than to PSH (0.3%). Taking the same 10% place, or $1.8 billion in PSH, would have a tendency to maneuver the inventory considerably and even be unattainable if Ackman needed to put money into a smaller firm on account of restricted float.

VCX owns at the very least double the variety of corporations as PSH. Nevertheless, about 75% of VCX is concentrated in OpenAI, Anthropic, Databricks, Anduril, dbt Labs, Vanta, Canva, and Ramp. So I might say the focus threat is much like PSH’s 8–12 corporations.

Conclusion Concerning the PSH Case Examine

I extremely doubt the Innovation Fund will commerce at the same {discount} to Pershing Sq. Holdings. They’re essentially completely different automobiles, with completely different asset bases, charge constructions, investor audiences, and structural dynamics. Though each are closed-end funds and lack the redemption mechanism of ETFs, the similarities largely finish there.

Pershing’s {discount} is primarily a perform of its public fairness publicity, closed-end construction with out a redemption mechanism, European itemizing frictions, efficiency charges, and focus threat. VCX, in contrast, offers entry to scarce non-public belongings, intends to listing in the USA, and doesn’t have a efficiency charge drag.

Whereas no listed car is immune from buying and selling at a reduction, making use of Pershing Sq.’s historic {discount} vary on to the Innovation Fund is probably going the improper framework.

Future Tech100 (DXYZ) and Robinhood Enterprise Fund (RVI)

A extra applicable comparability could also be DXYZ, which is presently buying and selling at roughly a 140% premium to its roughly $11.50 NAV, and the soon-to-be-listed RVI, the Robinhood Enterprise Fund.

Each maintain comparable hard-to-access non-public development corporations which might be in excessive demand. It is going to be telling to see whether or not RVI additionally trades at a premium to NAV following its $1 billion providing. If it does, the probabilities of VCX buying and selling at a premium goes up, and I’ll make investments extra in VCX pre-listing.

As we get nearer to RVI’s itemizing, I plan to publish a follow-up evaluation analyzing how its efficiency might inform expectations for the Innovation Fund. I’m doing this work primarily as a result of I’ve roughly $770,000 invested within the fund, which might realistically swing down by $150,000 or rise by as a lot as $385,000 merely primarily based on itemizing dynamics.

As a result of my spouse and I wouldn’t have day jobs, we rely closely on our investments to fund our life-style. As a DIY investor, I must conduct deeper due diligence to enhance the percentages of creating sound, long-term funding choices.

Anybody right here investing in Pershing Sq. Holdings? In that case, what are your ideas on how you can method the fund given its {discount} to NAV? Wouldn’t or not it’s higher to only put money into an S&P 500 ETF with minimal charges, provided that efficiency has been comparable over the previous 5–7 years?

Fundrise is a long-time sponsor of Monetary Samurai, as our funding philosophies are aligned. Please do your due diligence earlier than making any funding and solely make investments an quantity you possibly can afford to lose. There are not any ensures when investing in threat belongings, and you’ll lose cash.

{kind=link}