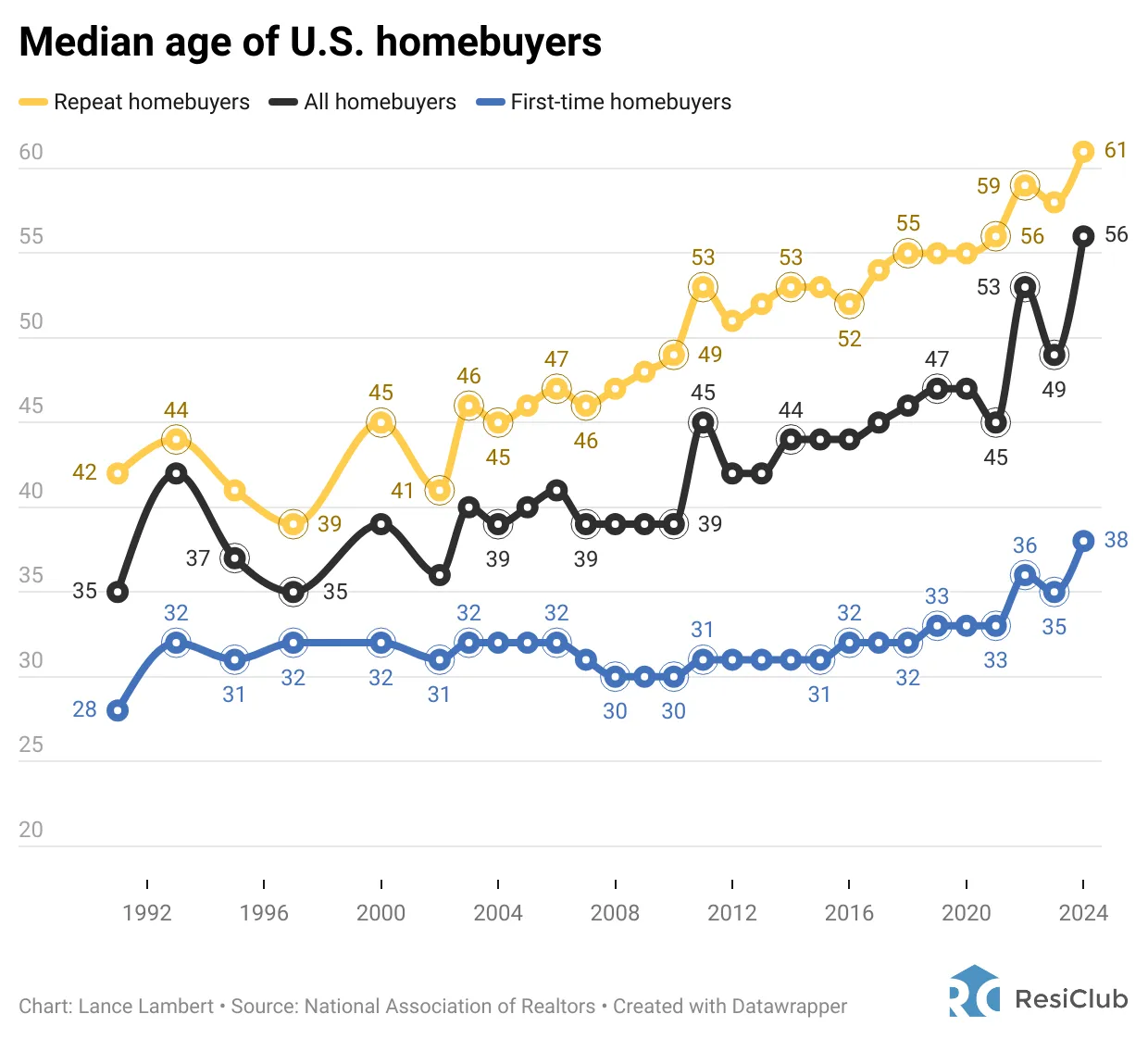

I just lately got here throughout an eye-opening chart by the Nationwide Affiliation of Realtors exhibiting that the median age of first-time U.S. homebuyers is now 38 years previous. That’s a big soar from 30 years previous between 2008 and 2010. In the meantime, the median age for repeat consumers has risen to 61 years previous.

What’s going on right here?

These numbers astound me as a result of life is way too brief to delay shopping for a house for that lengthy. After COVID, the median life expectancy within the U.S. is getting shorter, not longer. Most individuals purchase their first dwelling with the intention of settling down. But when you’re solely making this dedication at 38, you could not get to take pleasure in homeownership in the best way you had envisioned.

I perceive that rising dwelling costs and excessive mortgage charges are the primary components contributing to this development, making affordability more durable. Nonetheless, this publish is not focused at these the place affordability is their essential challenge.

As an alternative, this publish is directed at those that can afford to purchase a house, however look forward to the “good value” earlier than taking motion. The issue is that ready indefinitely can delay necessary life milestones, making it more durable to retire early, begin a household, and totally take pleasure in the advantages of homeownership.

Your Diminishing Hopes Of Retiring Earlier than 60

Ready for the right value to purchase a house can push again your retirement timeline considerably. If you buy your first dwelling at 38, you’ll possible take out a 30-year mortgage—in spite of everything, about 95% of homebuyers do, despite the fact that I choose an adjustable-rate mortgage (ARM) as an alternative. Matching your homeownership period with a decrease fixed-rate makes extra sense.

By the point your mortgage is paid off at 68, you could have already labored for 5 or extra years previous the standard retirement age. If you happen to had purchased a house at 28 as an alternative, you’ll have had a paid-off home by 58, permitting for a way more versatile and satisfying retirement.

In fact, some folks might need aggressively saved and invested between 18-38 to realize monetary independence earlier than shopping for a house. Nonetheless, that could be a smaller proportion of the inhabitants. Making a house buy at 38 typically means depleting a big amount of money and investments, probably reversing any monetary independence that they had achieved.

I skilled this firsthand after buying our dwelling in This fall 2023 with money from inventory and bond gross sales. This resolution induced my passive funding earnings to drop, leaving me on the worst level 25% wanting overlaying my desired family bills. Now, I have to spend the following 3-4 years making up for this deficit, delaying my monetary objectives.

Beginning A Household Might Be Extra Troublesome

Many individuals goal to purchase a house earlier than having youngsters, searching for stability earlier than increasing their household. Nonetheless, delaying homeownership could make it more durable to start out a household at an optimum age.

Fertility challenges improve after age 35, and ladies over this age are categorized as “geriatric” in maternity wards. My spouse and I skilled this firsthand through the births of each our youngsters in San Francisco. Many {couples} in our community additionally struggled with conception as they waited longer to quiet down.

If you happen to plan to purchase a house earlier than beginning a household however do not wish to threat fertility issues, I like to recommend starting your loved ones planning upon getting monetary stability and the appropriate associate, relatively than ready for the “good” dwelling buy.

A web value of no less than two occasions your gross family earnings is an affordable benchmark earlier than having youngsters. Basically, the larger your wealth earlier than having youngsters, the much less harassed you may be. Have a web value objective earlier than having children to maintain you centered.

In fact, it’s completely positive to start out a household and hire. Simply be sure you discover a place that’s owned by a landlord who desires long-term tenants.

The Flaws In Ready For The Excellent Worth

One of many largest causes folks delay homeownership is the idea that a greater value will come alongside. However market timing is almost unimaginable. Even when you accurately predict a market backside, you could battle to seek out the appropriate dwelling at the moment. And if the good dwelling does seem, likelihood is others shall be bidding on it, driving up the worth instantly.

As an alternative of attempting to time the market, purchase a house when you may afford to take action. If you happen to meet no less than two of my three home-buying guidelines within the 30/30/3 framework, you’re in place. Moreover, make sure you plan to personal the house for no less than 5 years as a consequence of excessive transaction prices.

Homeownership helps defend in opposition to inflation by stabilizing your housing prices. Renting indefinitely exposes you to hire will increase and instability. If you personal, you have got management over your dwelling scenario and may benefit from the safety of not being pressured to maneuver as a consequence of a landlord’s choices.

If you hire, your return on hire is at all times detrimental 100%. Sure, you get a spot to remain, however nothing extra. You don’t get the choice to dwell free of charge or truly generate income from shelter.

Different Examples The place Ready For A Higher Worth Can Be Detrimental

Being cost-conscious is necessary, however ready for the bottom potential value isn’t at all times one of the best monetary resolution. Listed below are different areas the place ready can negatively affect your high quality of life:

1. Emotional Nicely-Being & Relationships

Typically, spending extra for comfort—like taking a direct flight as an alternative of putting up with lengthy layovers—can considerably enhance your psychological and bodily well being. Hiring assist, equivalent to a nanny or home cleaner, can unencumber time to focus in your profession, household, or self-care. The price is well worth the lowered stress.

2. Medical Therapy

Well being is priceless. Delaying mandatory medical remedy in hopes of a decrease value can result in extreme issues, larger bills, and worse outcomes. Preventative care, common check-ups, and well timed therapies get monetary savings and lives in the long term.

3. High quality Time & Experiences

Touring with family members, attending milestone occasions, and creating lasting recollections are invaluable. Skipping experiences like taking your children to Disneyland or lacking out on a serious live performance to economize typically results in remorse. You possibly can at all times earn more cash, however misplaced time is irreplaceable. You possible gained’t be capable of hike the 20 mile Incan path in your 70s.

4. Profession & Enterprise Alternatives

A convention, course, or networking occasion may change the trajectory of your profession. Ready for a value drop may imply lacking out on key connections or profession development alternatives.

5. Important House or Automotive Repairs

A minor leak immediately can flip into main water harm tomorrow. A small automotive challenge can escalate into an costly breakdown. Ready for a “higher deal” on repairs typically leads to larger monetary losses down the highway.

6. Excessive-High quality Work Instruments

The fitting tools can considerably increase productiveness and earnings. A gradual laptop computer or outdated software program can waste hours of precious work time. I’m experiencing this firsthand with my 8GB MacBook Professional—it slows down always, killing my effectivity. A brand new one would pay for itself in improved productiveness, however I am unable to get myself to purchase a brand new one because it’s solely 5 years previous.

7. Schooling & Talent Growth

Investing in studying can result in larger lifetime earnings. A ebook on investing and private finance may yield hundreds in future features. Ready to save lots of $15 throughout a sale may end in misplaced alternatives value 1,000 extra.

8. Spending On Well being & Health

A great mattress, ergonomic chair, or gymnasium membership can forestall long-term well being points. Poor sleep or a sedentary life-style results in medical bills far exceeding the preliminary value of preventative measures. Are you actually going to sacrifice your sleep for 11 months to attend for that vacation mattress sale?

9. Childhood Milestones

Youngsters develop up shortly. Skipping significant experiences to economize—equivalent to extracurricular actions, holidays, or perhaps a high quality preschool—can imply lacking out on key developmental alternatives.

If there’s one other factor value spending cash on, moreover a nice major residence, it is in your children. As soon as they depart the home, 80% – 90% of the time you may ever spend with them shall be gone for good.

10. Hiring Expert Professionals

Whether or not for dwelling renovations, childcare, or monetary advising, ready for a lower cost can imply dropping entry to prime expertise. Expert professionals are in excessive demand, and the most cost effective possibility isn’t one of the best.

You Don’t At all times Have To Optimize For Financial savings – Pay Up For Comfort

As an alternative of at all times optimizing for financial savings, use your rising wealth to reinforce your life-style and comfort. Pay the additional 20 cents per gallon for gasoline as an alternative of driving 10 extra minutes to save lots of a couple of dollars. Select direct flights over layovers to save lots of time and cut back stress. Rent a home cleaner to unencumber hours for household, hobbies, or rest. Working towards the behavior of utilizing your wealth to enhance your life is simply as necessary as constructing it.

Earlier than shopping for my dwelling in 2023, I analyzed the chance of it coming again available on the market if I didn’t transfer ahead. The soonest potential resale could be mid-2025, primarily based on the vendor’s plans. His daughter was graduating highschool in 2025 and he talked about he’d wish to transfer again to his nation of origin.

Nonetheless, I couldn’t predict if the worth would nonetheless be inside attain. If the inventory market carried out properly in 2024 and 2025, demand may push costs even larger, making it more durable for me to purchase. On the identical time, if I purchased the home I might lose out on additional inventory market features. In the long run, I prioritized certainty over potential financial savings.

Though I most likely would have made more cash by ready, I’ve no regrets. I didn’t put my life or my household’s consolation on maintain for 2 years

What Are Your Ideas?

Are you shocked by the rising median age of homebuyers? How a lot of it is because of affordability versus ready for higher costs? What different areas of life have you ever seen folks delay for monetary causes, solely to comprehend it wasn’t value it? Let me know your ideas!

Diversify Into Excessive-High quality Non-public Actual Property

Shares and bonds are traditional staples for retirement investing. Nonetheless, I additionally counsel diversifying into actual property—an funding that mixes the earnings stability of bonds with larger upside potential.

Take into account Fundrise, a platform that means that you can 100% passively spend money on residential and industrial actual property. With nearly $3 billion in personal actual property property underneath administration, Fundrise focuses on properties within the Sunbelt area, the place valuations are decrease, and yields are typically larger.

With a strong economic system, a robust inventory market, pent-up demand, and engaging costs, I anticipate industrial actual property costs to proceed to get well. I’ve personally invested over $300,000 with Fundrise, and so they’ve been a trusted associate and long-time sponsor of Monetary Samurai. With a $10 funding minimal, diversifying your portfolio has by no means been simpler.

Subscribe To Monetary Samurai

Hear and subscribe to The Monetary Samurai podcast on Apple or Spotify. I interview consultants of their respective fields and focus on a few of the most fascinating subjects on this website. Your shares, rankings, and opinions are appreciated.

To expedite your journey to monetary freedom, be a part of over 60,000 others and subscribe to the free Monetary Samurai publication. Monetary Samurai is among the many largest independently-owned private finance web sites, established in 2009. Every little thing is written primarily based on firsthand expertise and experience.

{kind=link}