Excessive-yield dividend shares could be a highly effective technique to generate regular revenue – and some are providing payouts that crush the market common.

Funding companies Jefferies and BTIG have just lately pointed to 2 such names that stand out. Each provide dividend yields approaching 10% – about seven instances larger than the S&P 500 common.

Nonetheless, diving into high-yield shares requires additional diligence. Whereas they will provide enticing revenue, they might additionally include elevated dangers, resembling potential dividend cuts or underlying enterprise challenges.

That’s why we turned to the TipRanks database to see whether or not the remainder of Wall Avenue is backing these picks. Right here’s what we discovered.

Blue Owl Capital Company (OBDC)

We’re beginning with a BDC – brief for Enterprise Improvement Firm. These corporations step in the place conventional banks typically gained’t, providing capital and credit score to rising companies that energy the U.S. financial system. Blue Owl Capital Company (OBDC) is a key participant right here, offering financing and credit score providers to the sorts of companies which have lengthy served because the nation’s financial engine.

OBDC is managed by Blue Owl Credit score Advisors, an arm of Blue Owl Capital Inc., and it makes a speciality of financing middle-market corporations. The agency takes a debt-first strategy, with a selective eye towards fairness, constructing a portfolio that now spans 236 companies with a mixed truthful worth of $17.7 billion. The common funding measurement is $75 million.

Wanting on the drill-downs, we discover that the corporate’s portfolio is made up primarily of first-lien senior secured loans, at ~76% of the full. Widespread fairness makes up ~12%, and second-lien senior secured loans make up ~5%. Of the full portfolio, 96.5% of the property are floating fee, and the rest are mounted. OBDC invests in a variety of enterprise sectors, and greater than half of its investments are within the Southern and Western areas of the US.

Financially, the corporate reported adjusted web funding revenue of $0.39 per share in Q1 2025. That got here in beneath expectations, lacking forecasts by 4 cents.

The common dividend was declared at 37 cents per share, and was accompanied by a supplemental cost of 1 cent per share. The common dividend annualizes to $1.48 per share and provides a ahead yield of 10.7%.

Jefferies analyst Matthew Hurwit covers this BDC, and he’s impressed by the corporate’s potential to ship returns.

“We view OBDC as a compelling revenue funding with a base-case complete return pushed by a double-digit dividend yield and modest NAV/share progress. In an upside situation, continued sturdy credit score efficiency and elevated investor recognition might end in a number of enlargement (worth/NAV transferring to a premium), delivering extra capital good points. In a draw back situation, a fabric financial downturn might strain portfolio corporations and valuations; nevertheless, OBDC’s conservative portfolio (83% senior secured loans) and low non-accruals ought to assist mitigate losses. Total, OBDC’s giant scale, prudent underwriting, and help from Blue Owl’s platform underpin a positive risk-adjusted return profile for income-focused traders,” Hurwit opined.

Hurwit goes on to place a Purchase ranking on OBDC shares, and his $16 worth goal implies a one-year upside potential of 15%. Add within the common dividend yield, and this inventory’s complete one-year return could attain as excessive as 25.7%.

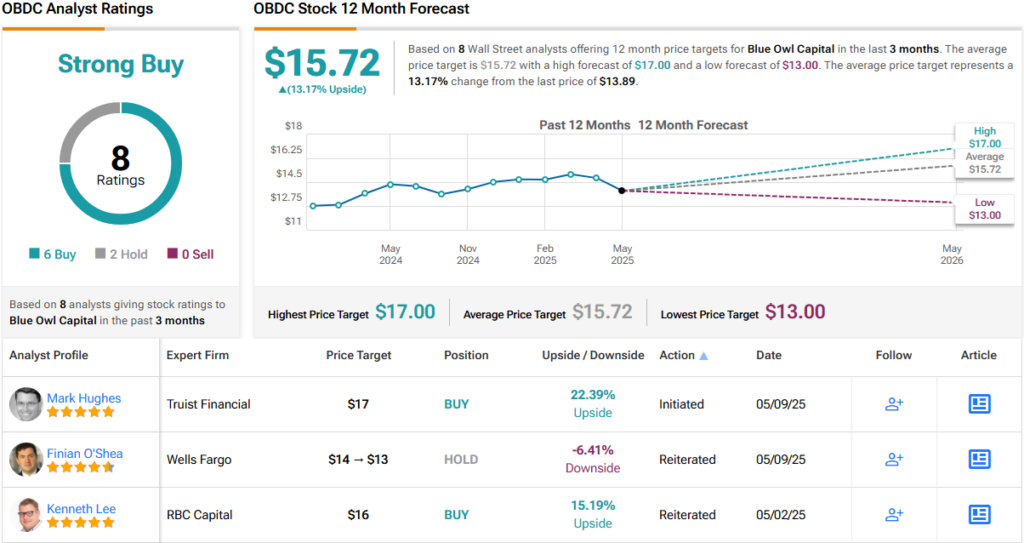

Total, OBDC has a Sturdy Purchase consensus ranking from the Avenue’s analysts, primarily based on 8 current opinions that embody 6 Buys and a pair of Holds. The shares are priced at $13.89, and their $15.72 common worth goal implies 13% upside potential. (See OBDC inventory forecast)

Apollo Business Actual Property (ARI)

Subsequent up is a REIT, or actual property funding belief. These corporations are well-known as dividend champs; dividend funds make a handy automobile for compliance with tax rules to return earnings on to shareholders. Apollo Business Actual Property operates within the US and Europe, the place it each originates and invests in business actual estate-related debt investments, together with senior mortgages and mezzanine loans. The corporate’s portfolio is collateralized by properties, and as of this previous March 31, it had an amortized price of $7.7 billion.

Apollo Business Actual Property is externally managed by an oblique subsidiary of the choice funding supervisor, Apollo International Administration. The bigger world asset supervisor has invested greater than $105 billion into business actual property since 2009, and $26 billion of that complete was invested on behalf of Apollo Business Actual Property. Apollo Business Actual Property makes use of its relationship with the bigger asset supervisor to understand benefits in its enterprise, in sourcing, evaluating, underwriting, and managing its investments in business actual property.

Apollo Business Actual Property’s portfolio comprises 48 loans, primarily floating-rate and mortgage loans. The weighted common remaining time period of the loans is 2.4 years. The portfolio is various, with 24% in workplace house, one other 24% in residential properties, and 21% in lodges. Of the rest, 12% is in retail properties. Geographically, 32% of the portfolio is within the UK and 20% is in New York. The following largest geographic segments of the portfolio are Europe, at 17%, and the American Southeast, at 11%.

On the monetary aspect, Apollo Business Actual Property final reported outcomes for 1Q25. In that quarter, the corporate realized a web revenue attributable to frequent shareholders of 16 cents per share. The corporate’s distributable earnings per diluted share got here to 24 cents. On April 15, the corporate paid out a standard share dividend of 25 cents; the annualized fee of $1 per frequent share provides a ahead yield of 10.4%.

This inventory has caught the attention of BTIG analyst Tom Catherwood, who notes that the corporate is agile, and able to shifting its portfolio stance to satisfy altering circumstances.

“Whereas now we have been optimistic on ARI’s platform for a while, we feared that large-scale challenged loans (specifically Steinway Tower and a portfolio of hospitals in MA) might require the corporate to retain extra capital, limiting its skill to constantly originate and develop its mortgage ebook. That stated, ARI swiftly resolved its MA hospital mortgage publicity, and given current gross sales exercise at Steinway, we count on the corporate to begin amassing revenue on its $288M senior mezz mortgage on the property in 2Q25. Given a more healthy place in Steinway, regular mortgage origination pipeline, institutional backing from Apollo International Administration, and platform within the UK/Europe (52% of the mortgage ebook), we imagine ARI is positioned to outperform its peer group throughout a time of volatility for the US business actual property market,” Catherwood defined.

Catherwood’s feedback help his Purchase ranking on ARI shares, whereas his $11 worth goal means that ARI will acquire 14.70% going ahead. With the dividend yield, this inventory’s complete return could attain 16%. (To observe Catherwood’s monitor document, click on right here)

That’s one aspect of the Avenue. The broader analyst consensus takes a extra cautious stance, touchdown at Maintain (i.e., Impartial). Out of 6 current rankings, there are 2 Buys, 3 Holds, and 1 Promote. With shares buying and selling at $9.59 and a median worth goal of $9.80, that factors to a extra muted upside of two% over the following 12 months. (See ARI inventory forecast)

To search out good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Finest Shares to Purchase, a instrument that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is vitally essential to do your individual evaluation earlier than making any funding.

{kind=link}