I’ve mentioned it earlier than, I’ll say it once more: For my part, Warner Music Group made two important strategic missteps over the previous 20 years.

The primary was an under-investment in unbiased distribution. Living proof: in the identical yr Sony Music introduced it was spending $400+ million to purchase AWAL, Warner splashed a comparable sum on 300 Leisure, which has since been denuded all the way down to an Atlantic A&R hub.

WMG’s second mistake was its under-investment in catalog M&A. As Larry Mestel‘s Main Wave was amassing its battle chest, as Merck Mercuriadis was constructing Hipgnosis, as non-public fairness began pouring billions into music rights, Warner largely stood nonetheless.

As Mestel as soon as informed me: “Again in 2006, had the majors been aggressive, not one of the corporations that you just’re speaking about would have ever been in a position to get into the enterprise, together with us.”

Since Robert Kyncl took over as WMG CEO in 2023, he’s earned his justifiable share of business brickbats. Sweeping Warner layoffs proceed to be whispered about at business dinners. And the previous YouTube exec’s vocabulary can definitely give off the bouquet of a tech-head, fairly than a ‘music man’.

But Kyncl is not less than making an attempt to instantly tackle each of Warner’s historic shortfalls.

On catalog: Warner’s three way partnership with Bain Capital has now deployed $650 million on acquisitions, led by the Pink Scorching Chili Peppers’ masters at $300 million-plus. The automobile has been upsized from $1.2 billion to $1.65 billion.

On indie distribution: WMG’s current acquisition of Revelator – a cloud-based platform for independents – is a small however direct problem to FUGA (beneath UMG/Virgin Music Group).

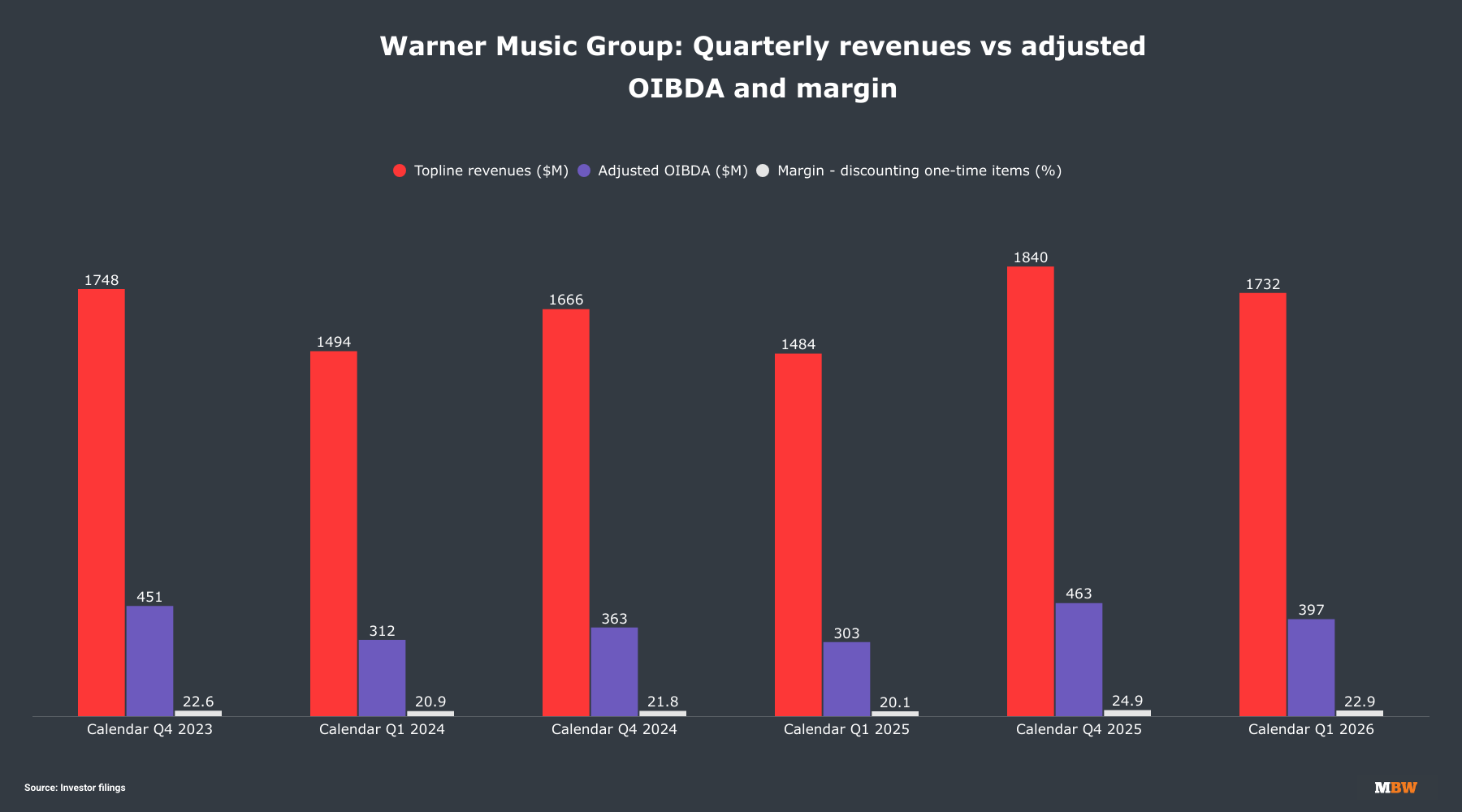

On the similar time, Warner simply had certainly one of its most spectacular quarters in years. The corporate generated $1.73 billion in calendar Q1, up by practically $250M vs the prior-year interval (albeit comped towards a dud of 1 / 4 in 2025).

The temper on WMG’s newest earnings name, held on Could 7, was jubilant. Kyncl opened the Q&A part with this comment: “After years of doing onerous, unsexy foundational work, after making robust organizational choices and redesigns… we’ve got now hit our stride. It feels actually good to be at Warner right now.”

Listed below are three issues value contemplating about Warner Music Group’s technique, and its place out there, as issues stand…

1) Warner’s margin transformation is actual – and the goal is formidable

On the Could 7 earnings name, CFO Armin Zerza – who was concurrently promoted to CFO/COO – was blunt about the place Warner’s profitability has been, and the place it’s headed:

“Frankly, our margins have been means too low [in the past]. Once I began right here, it was within the low 20s. As you possibly can see, fiscal year-to-date, we’re round 24%… I’m very assured that we will get to the high-20s goal within the medium to long run.”

The excessive 20s – i.e., approaching 30%. Zerza is speaking a couple of structural transformation of Warner’s economics, not a one-quarter sugar rush.

At a JPMorgan convention earlier this week, Zerza went additional.

He credited WMG’s margin positive factors to 3 elements: “One, centered on what we name ‘worthwhile progress’… Quantity two, value financial savings that was primarily pushed by a reorganization of the corporate from what was a really native group to a global-regional-local group. And… now, clearly, working leverage.”

He highlighted a specific stat value contemplating: catalog, mentioned Zerza, accounts for 65% of WMG’s recorded music streaming income right now – and infrequently carries 50%+ margins.

He added: “Lower than 5% of our songs [today] characterize greater than 90% of our income on DSPs. That provides you the thought of how concentrated client habits actually is in music.”

This stat contrasts with figures introduced by then-Warner CEO, Steve Cooper, 4 years in the past, when Cooper heralded an period of lessening famous person focus in WMG’s enterprise.

Mentioned Cooper: “[In 2012] our High 5 artists generated over 15% of our recorded music bodily and digital income. In 2022, they generated simply over 5%.”

If I needed to guess, the re-concentration of Warner’s revenues right into a relative handful of hit artists has been pushed by one factor: the market share explosion of evergreen catalog music.

Don’t neglect: the whole streaming quantity of latest music really fell in actual phrases within the US final yr – down 5 billion streams YoY – as catalog music surged.

2) Robert Kyncl’s ’empty energy’ philosophy – and an intriguing declare about distribution

Robert Kyncl has beforehand mentioned that Warner strategically avoids “empty energy” offers – aka distribution agreements that ebook massive revenues however skinny earnings.

He counted Warner’s former world distribution settlement with BMG as one such deal, and didn’t shed tears when it ended. Kyncl additionally wasted little time dumping Warner’s DIY distribution platform, Stage Music, quickly after becoming a member of the corporate.

This “empty energy” philosophy is central to understanding how Warner thinks about indie distribution in 2026 – a sector broadly considered structurally lower-margin than frontline label operations.

On the Could 7 WMG earnings name, Kyncl made a placing declare about Alejandro Duque, who now runs ADA alongside Warner’s Latin America operation.

LATAM, Kyncl famous, is a “very distribution-heavy market.” Then he mentioned: “[Duque] has managed to run that territory on a margin which is [broadly] the identical as our firm’s.”

This declare was repeated by Armin Zerza this week, who mentioned that Duque’s group had “grown [WMG’s LATAM] enterprise on common 15% each single yr for the previous 5 years at virtually firm common margins“.

It’s a notable assertion: regardless of indie distribution offers remaining the bedrock of the Latin market, WMG’s LATAM enterprise is seemingly banking someplace close to the mid-20-percent OIBDA margins exhibiting up within the agency’s world numbers.

Duque’s remit in Latin America goes far past indie distribution, after all, encompassing frontline label exercise and different income strains. And Warner doesn’t particularly escape margins for ADA in its fiscal filings, so we will’t know for certain the place they sit.

However this can be a pattern value watching at Warner. In an business the place indie distribution is more and more the place the expansion is, the query of how worthwhile that progress is issues.

One different view? There are methods to develop margins in indie distribution past watching the pennies.

The vast majority of offers at Sony‘s The Orchard or UMG’s Virgin Music Group, for instance, will inevitably be lower-margin than offers at their sister document corporations. But these companies usually leverage their relationships with mentioned indies to make fairness investments into their companies, thereby boosting margins.

A worldwide indie distribution/administration community may also act as a far-reaching catalog M&A pipeline, giving priceless visibility into market alternatives.

As Chord Music’s John Chapman mentioned this week of Chord’s relationship with UMG: “[Chord] had a terrific partnership with the group at KKR for a few years, however the actuality is that in that point interval, I purchased eight catalogs for roughly $350 million. Then final yr, [having established a partnership with UMG], I purchased 20 catalogs for $800 million.

“It’s only a clear, elementary distinction – a pipeline of alternatives that I see as a direct results of our partnership with UMG.”

3) In a means, Warner is hanging again within the majors’ race. In one other means, it’s changing into extra distinctive.

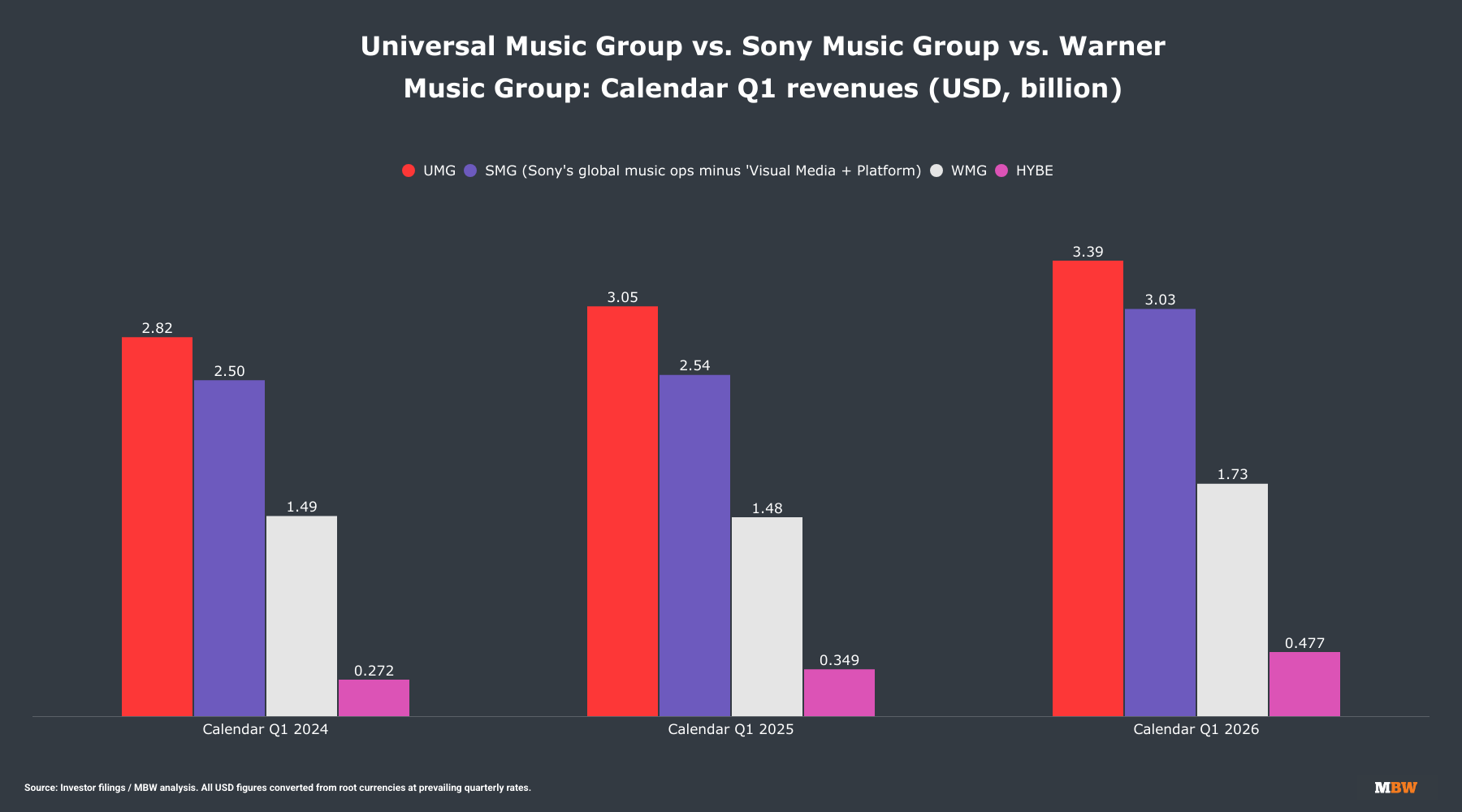

The chart beneath reveals calendar Q1 revenues for UMG, Sony, Warner, and HYBE, over the previous three years. All figures are in USD, transformed from root currencies the place required at prevailing quarterly charges.

From calendar Q1 2024 to calendar Q1 2026, UMG added practically $600 million in quarterly income. Sony added roughly $500 million. Warner added nearer to $250 million.

Because of this, the quarterly income hole between the No.2 and No.3 main widened throughout this era, from ~$1.0 billion in Q1 2024 to ~$1.3 billion in Q1 2026.

In the meantime, in gross income phrases, UMG stays roughly double the dimensions of WMG right now.

There was a time when Warner’s publicly acknowledged ambition was to catch the No.2 participant within the world market. Former CEO Steve Cooper informed me as such.

These days have gone: in gross income phrases, the probability that Warner can in the future break into the ‘huge two’ appears pretty much as good as over.

But that may not be the proper lens by way of which to view WMG anymore.

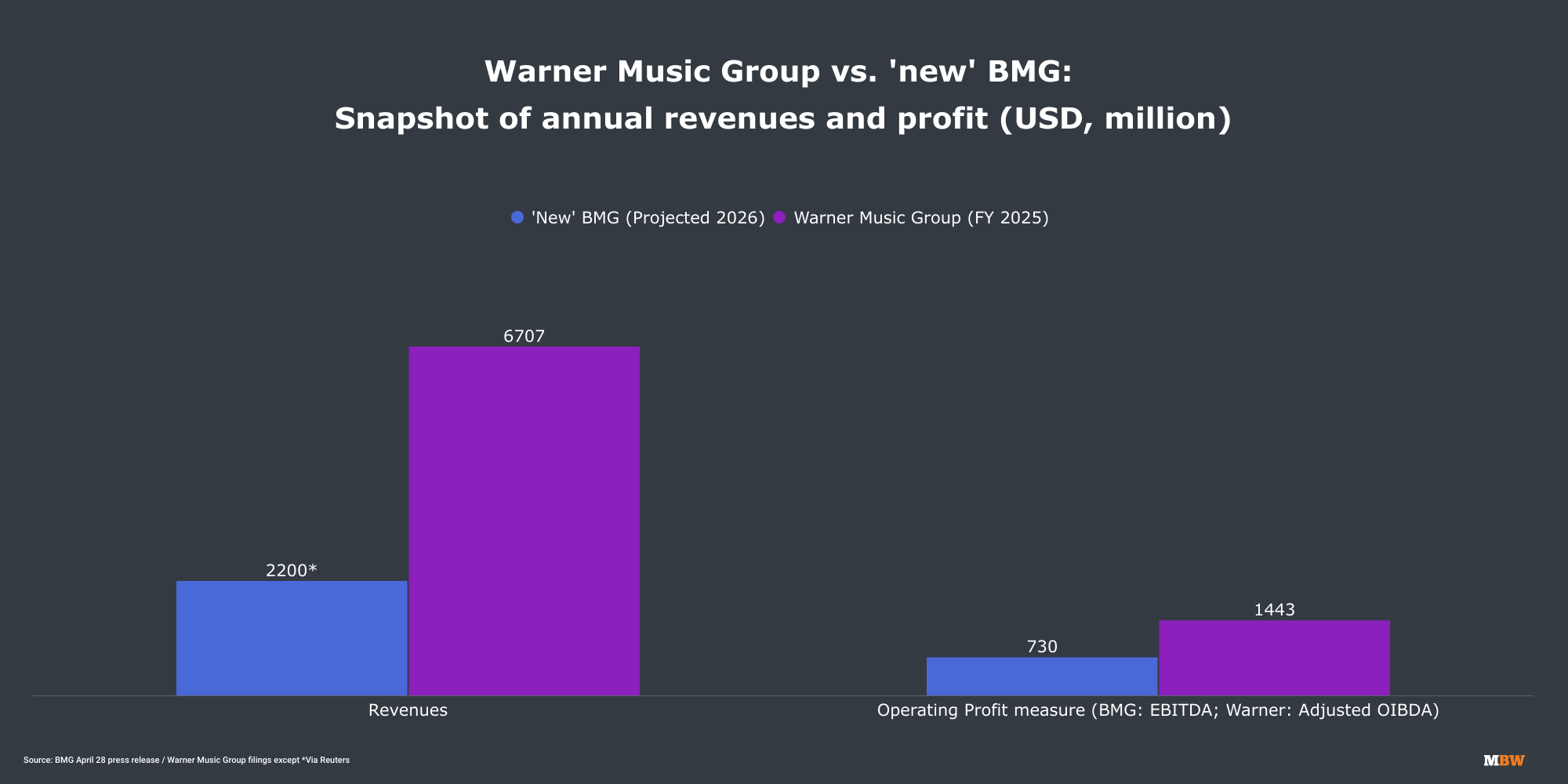

Warner is quietly changing into one thing else: an organization too huge to be referred to as an ‘unbiased’, working at a number of occasions bigger than HYBE or the soon-to-be-merged BMG/Harmony (valued at roughly $15 billion on a projected $730 million annual EBITDA).

But Warner is combining this distinctive No.3 market energy with its ever-increasing thirst for margin.

Armin Zerza described WMG’s method at JPMorgan this week as a “flywheel”: margin enchancment generates money, money funds funding, funding drives progress, progress expands margins additional.

He mentioned Warner has been in a position to “develop the enterprise whereas really spending much less in A&R as a p.c of income.”

WMG is doing this whereas nonetheless growing its A&R spend YoY in actual phrases.

That’s not an organization attempting to outspend its competitors. It’s an organization attempting to out-earn them, per greenback invested.

Which brings me to essentially the most provocative second from Zerza’s JPMorgan look this week.

Requested in regards to the hole between private-market multiples for music catalogs and public-market valuations for music corporations, he was blunt: “We agree that our public valuation doesn’t mirror our underlying worth, particularly given the outcomes that we’ve got been delivering and can proceed to ship.”

Zerza then added: “Pretty refined traders around the globe agree… you’ve heard that just lately from one massive investor as they checked out our business.”

That was a nod to Invoice Ackman’s Pershing Sq., which in April launched a bid to amass Common Music Group at a $64 billion valuation – partly on the thesis that public markets are chronically undervaluing UMG’s inventory.

Len Blavatnik‘s Entry Industries took Warner Music Group non-public for $3.3 billion in 2011. It then floated the corporate on the Nasdaq in 2020. Immediately, Warner’s market cap sits at roughly $18 billion.

If Zerza is correct that public markets don’t mirror Warner’s underlying worth… and if Ackman is correct that the music business’s greatest days are forward of it… and if Blavatnik agrees with each…

May Warner find yourself as a non-public firm once more over the following few years? Maybe a form of catalog-heavy, world ‘enormo-indie’, with a 30%-plus margin profile? I gained’t be shocked if that’s the last word vacation spot.Music Enterprise Worldwide

{kind=link}