The U.S. Division of Well being and Human Providers defines childcare as reasonably priced if it prices 7% or much less of a household’s earnings. But, in each single state, the standard household far exceeds that threshold, qualifying them as “cost-burdened” by this important service.

The timing couldn’t be worse as 1 in 3 owners and 1 in 2 renters are presently thought-about cost-burdened by housing—placing the 2 greatest and most important prices of a household funds into direct competitors.

“Households with younger youngsters are dealing with this double whammy,” explains Yulia Panfil, director of the Way forward for Land and Housing Program at New America, a assume tank. “If they do not pay for youngster care, then they cannot work, and if they cannot work, then they cannot pay lease. So it is this vicious cycle.”

And it is a dire evaluation of the truth households face right now. As a scarcity of 4.03 million houses collides with a scarcity of 4.2 million childcare slots, advocates argue these crises at the moment are inextricably intertwined.

The price of costly childcare and housing

The clearest connection between housing and childcare prices is discovered within the demographic most susceptible to dropping their houses.

Minors face the best danger of eviction within the U.S., based on analysis from the Eviction Lab. They account for roughly 40% of all people threatened with displacement yearly. Moreover, households with kids characterize over half (52%) of all eviction filings.

“Practically 3 million youngsters are on the receiving finish of an eviction discover every year, which is simply surprising,” says Panfil. “For therefore many households, their two largest family funds gadgets are lease and childcare. And in cities like DC, the place I dwell, the price of childcare really is larger than the price of lease for a lot of, and that is per youngster.”

That information is a stark illustration of the not possible trade-off essentially the most cost-burdened households face: Pay for childcare so you possibly can work, however then fall quick on lease; or pay the lease, however lose your capability to work as a result of you possibly can’t afford the childcare.

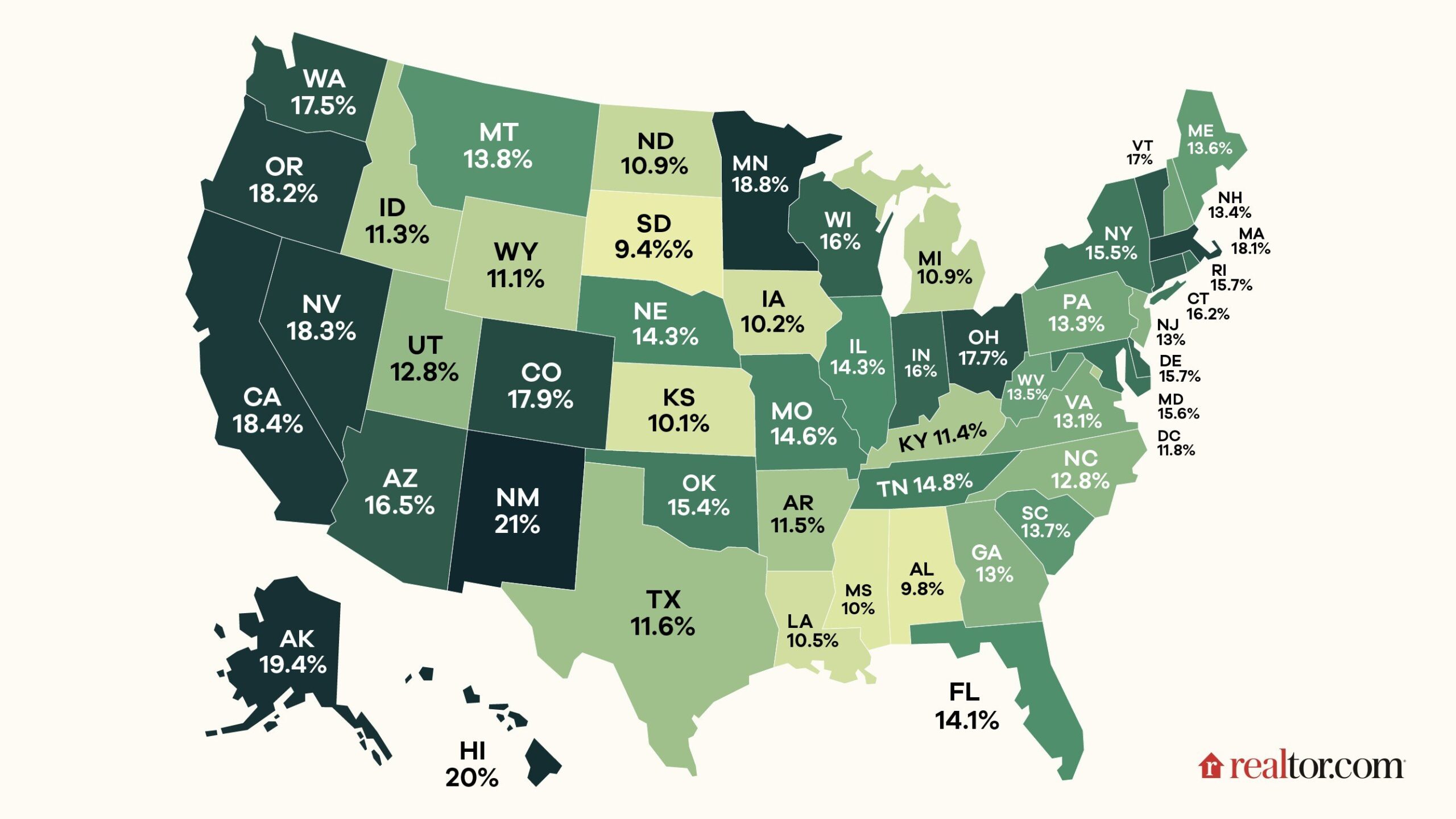

The place households are essentially the most cost-burdened by childcare

Knowledge from the Financial Coverage Institute (EPI) exhibits {that a} median-income household in each state exceeds the 7% childcare affordability threshold by 2 to six share factors. For minimum-wage staff, the burden is much more extreme—starting from 29 to 108 share factors.

Elise Gould, a senior economist on the EPI, started noticing a troubling shift within the information a decade in the past.

“Abruptly, childcare turned dearer than housing in plenty of counties throughout the nation,” she says. “It actually shocked us.”

Right this moment, her analysis exhibits that toddler care prices greater than in-state faculty tuition in 29 states and the District of Columbia.

Joel Berner, senior economist at Realtor.com®, says that these pressures are hitting the housing market, too.

“We’re seeing it within the battle of first-time homebuyers,” he says. “This group is of the age that they’re delicate to each mortgage charges (most do not already personal a house) and childcare prices, and so they’re getting squeezed within the West and in coastal markets.”

When analyzing how a lot of a median household’s earnings is consumed by the mixture of a typical mortgage and toddler care—it is these areas within the Western and coastal markets that stand out. Hawaii, California, and Massachusetts are affected essentially the most.

“Saving for a down fee is the very best factor a first-time purchaser can do on this surroundings, however when different prices like childcare are too excessive as nicely, there’s not a lot left after the payments are paid,” he provides.

The maths is even brutal for individuals who’ve been in a position to break into the market.

In Hawaii, which ranks because the sixth most costly state for toddler care, childcare alone consumes 20% of a median household’s earnings, then including a typical mortgage fee brings that whole to 75% of their earnings.

In the meantime, California ranks fourth for toddler prices, then including the standard mortgage on high of childcare consumes greater than 71% of the standard household’s earnings.

The identical is true in Massachusetts, which ranks because the second most costly place for childcare. However the math is so restrictive within the Bay State that solely 8% of households within the state can afford toddler care with out being cost-burdened.

And whereas these figures characterize typical households on the median earnings, the squeeze is way extra acute for minimum-wage staff.

In New Hampshire and Wisconsin, childcare prices alone would devour 115% and 112% of a employee’s whole earnings, respectively.

In a merciless twist, Gould notes that childcare staff are sometimes essentially the most acutely burdened by the disaster they assist handle.

“Childcare staff are those which might be doing this invaluable work to handle our youngsters, and so they themselves are paid such low wages, and so they’re undervalued for that work, that they cannot afford childcare themselves,” she says.

On common, childcare staff must spend between 30% and 74% of their earnings on childcare alone—earlier than even contemplating the price of housing.

The identical pressures driving up housing are driving up childcare prices

The truth that childcare prices have risen in close to lockstep with dwelling costs isn’t any coincidence. For a lot of childcare suppliers, their largest mounted value is lease—and as industrial and residential property values have surged, these overhead prices are handed on to households.

That shift has hit residential suppliers—typically essentially the most reasonably priced and versatile choices for households—notably laborious.

“Operating a childcare enterprise isn’t one thing that one does for an enormous revenue, and so the smallest change can actually have ripple results,” explains Erica Meade, coverage director of the New Apply Lab at New America. “If their lease is larger or their insurance coverage is larger, it has to get handed on to households, or they eat it.”

As extra of those suppliers have closed, that’s additionally created shortage, which in flip drives up prices.

Right this moment, greater than half of the U.S. inhabitants (51%) lives in a childcare desert, outlined by the Middle for American Progress as a census tract with greater than 50 kids underneath age 5 and both no childcare suppliers or so few choices that there are greater than thrice as many kids as licensed childcare slots.

As if that wasn’t sufficient, childcare facilities are dealing with an insurance coverage disaster of their very own in one other mirror to the skyrocketing premiums which might be hitting some housing markets laborious.

Samantha Phillips, an early training insurance coverage agent and advocate, says that she’s watched premiums swell from round $10,000 per 12 months for the standard web site in 2023 to greater than $25,000 per 12 months right now. And in high-risk areas or websites which have had claims prior to now, insurance policies can value as a lot as $45,000 to $75,000 a 12 months per web site.

In each dialog for this text, one theme was clear: Households are in a second of disaster as a result of the industries they depend on are in disaster. To supply reduction to 1 would require providing reduction to all.

As Phillips put it: “I really feel like I’ve spent the final three years actually screaming from the mountaintops that doomsday is coming and doomsday is right here, and doomsday is getting worse.”

{kind=link}