As of closing bell on Might 29, the S&P 500, Nasdaq Composite, and Dow Jones Industrial Common have every generated roughly breakeven returns on the 12 months. Usually, returns this mundane would not be celebrated. However when you think about that every of the key inventory market indexes declined by double digits only a month in the past, getting again to even looks like a win.

Powered by Cash.com – Yahoo might earn fee from the hyperlinks above.

One of many extra fascinating facets of the worth motion within the inventory market this 12 months is annotating exactly when main volatility occurred. In keeping with just lately printed knowledge, it seems that the market’s most pronounced declines and positive factors all through 2025 will be traced again to main bulletins from Washington, D.C.

Going somewhat deeper, every time President Donald Trump has introduced new tariff insurance policies, the market reacted negatively. However when he has eased the strain, shares skilled sharp rebounds. This dynamic has grow to be often known as the TACO commerce — which stands for “Trump all the time chickens out.”

Contemplating the tariff state of affairs continues to be very a lot ongoing, I think the capital markets will proceed working below heightened ranges of uncertainty. Nonetheless, I see two no-brainer synthetic intelligence (AI) shares that appear to be nice buys proper now — no matter TACO commerce volatility. In spite of everything, buying and selling primarily based on what you suppose Trump might or might not do subsequent is a short-term and dangerous method to investing, however specializing in strong long-term alternatives amid the chaos is a sensible selection.

Let’s discover which shares good traders might need to contemplate shopping for the dip in because the TACO commerce continues to make waves.

The primary AI inventory on my listing is semiconductor king Nvidia(NASDAQ: NVDA). Not solely does Nvidia dominate the marketplace for high-performance chipsets often known as graphics processing items (GPUs), however the firm’s general efficiency has basically grow to be the last word barometer by which the AI business is measured. Mentioned otherwise, if Nvidia’s enterprise is rising, traders have a tendency to stay bullish on the AI increase.

From a macro standpoint, Nvidia stands to profit from ongoing funding in AI infrastructure. As long as cloud hyperscalers Amazon, Microsoft, and Alphabet, in addition to tech titans like Meta Platforms, Oracle, and Apple, are constructing out knowledge facilities and shopping for chips, Nvidia is positioned to seize a portion of this multitrillion-dollar alternative.

So far as tariffs go, the most important menace to Nvidia’s enterprise proper now’s its restricted alternative in China. New export controls coupled with rising competitors from China-based Huawei has put Nvidia in a tricky spot. Nonetheless, Nvidia has alternatives to maneuver round China-related headwinds.

As an illustration, the corporate just lately received a number of contracts within the United Arab Emirates (UAE) Kingdom of Saudi Arabia (KSA) — every of which will likely be outfitting AI knowledge facilities with Nvidia’s newest Blackwell GPUs. Furthermore, rumors are swirling that Elon Musk’s AI start-up, xAI, may very well be buying an estimated $40 billion price of chips for its subsequent GPU cluster.

As I beforehand predicted, I believe Nvidia inventory goes to rebound significantly all through the latter half of 2025 as I think tariff-driven fears will subside.

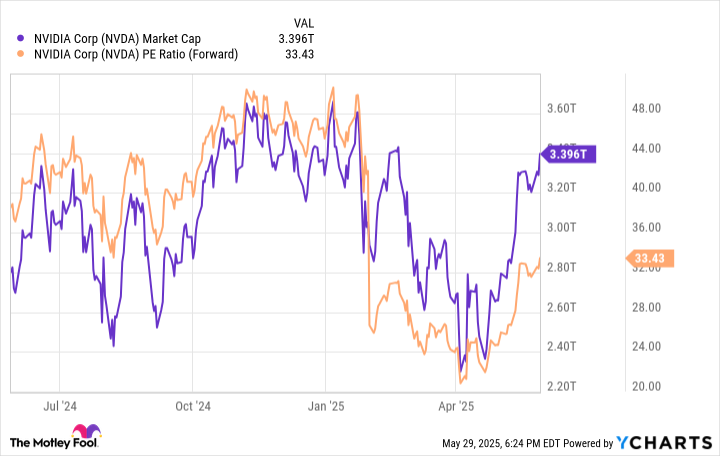

Whereas there was some latest valuation growth following Nvidia’s monster first-quarter earnings report, the inventory nonetheless seems affordable in comparison with historic ranges on a ahead price-to-earnings (P/E) foundation.

Picture supply: Getty Photographs.

Subsequent up on my listing is Amazon. On the floor, this would possibly appear to be a head-scratcher. I will concede that Amazon’s core e-commerce enterprise is fairly weak to tariffs.

Nonetheless, I am not distracted by these headwinds in the mean time.

As a substitute, I have been analyzing Amazon primarily based on two different areas of the enterprise. First, the corporate’s cloud infrastructure unit, Amazon Net Companies (AWS), continues to speed up gross sales and widen working margins. To me, this alerts that the corporate’s investments in AI have, thus far, paid off.

What’s extra profitable, nonetheless, is that AWS accounts for almost all of working income for Amazon’s whole enterprise. That is essential, as a result of even throughout a time of financial uncertainty, the efficiency from AWS has remained robust and continued minting heaps of money circulate for Amazon. These sturdy unit economics present Amazon with a excessive diploma of working leverage — permitting the corporate to double down and reinvest in high-growth areas.

In flip, Amazon has a novel skill to sew extra AI-driven investments throughout the broader material of its ecosystem — from e-commerce, logistics, brick-and-mortar retail, promoting, streaming, subscription providers, and even direct-to-consumer healthcare.

It is these dynamics which will have caught the attention of billionaire hedge fund supervisor Invoice Ackman, who just lately joined Warren Buffett and Cathie Wooden in including Amazon to his portfolio.

I believe Amazon is properly on its technique to changing into Wall Avenue’s first $5 trillion firm. Whereas the corporate might face some turbulence within the close to time period because of tariffs, this isn’t the primary time the tech large has handled a difficult regulatory surroundings. But, in the long term, Amazon has continued to handle to diversify its platform and construct a variety of multibillion-dollar companies profitability.

I see Amazon as an under-the-radar alternative proper now and I’d benefit from any dips because the TACO commerce performs out.

Before you purchase inventory in Nvidia, contemplate this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they consider are the 10 greatest shares for traders to purchase now… and Nvidia wasn’t one in all them. The ten shares that made the reduce might produce monster returns within the coming years.

Contemplate whenNetflixmade this listing on December 17, 2004… when you invested $1,000 on the time of our suggestion,you’d have $651,049!* Or when Nvidiamade this listing on April 15, 2005… when you invested $1,000 on the time of our suggestion,you’d have $828,224!*

Now, it’s price notingInventory Advisor’s complete common return is979% — a market-crushing outperformance in comparison with171%for the S&P 500. Don’t miss out on the most recent prime 10 listing, out there once you be part ofInventory Advisor.

Suzanne Frey, an government at Alphabet, is a member of The Motley Idiot’s board of administrators. Randi Zuckerberg, a former director of market improvement and spokeswoman for Fb and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Idiot’s board of administrators. John Mackey, former CEO of Entire Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Adam Spatacco has positions in Alphabet, Amazon, Apple, Meta Platforms, Microsoft, and Nvidia. The Motley Idiot has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Oracle. The Motley Idiot recommends the next choices: lengthy January 2026 $395 calls on Microsoft and brief January 2026 $405 calls on Microsoft. The Motley Idiot has a disclosure coverage.

{kind=link}